By Marsha McGraw Olive

Marsha McGraw Olive, PhD, retired from the World Bank in 2015 as Country Manager of Tajikistan capping a quarter-century career in the Europe and Central Asia region. Earlier positions included postings in Moscow as Acting Country Director and in Bratislava, Slovakia. During an external assignment she served as Senior Vice President of the Eurasia Foundation, where she managed a small grant program in the twelve countries of the former Soviet Union. From 2015-2016 she taught at Bahçeshehir University in Istanbul, Turkey. She is currently on the faculty of European and Eurasian Studies at Johns Hopkins SAIS, where she received the Excellence in Teaching Award for 2019-20 as Outstanding Adjunct. Her substantive expertise comprises Russian and Eurasian studies, comparative political economy, and security policy.

In April 2020, cabbages rotted on the roadside as trucks, delayed by closed borders, dumped their freight on the road from Kazakhstan into the Kyrgyz Republic. Aside from being a human health crisis, a major casualty of COVID-19 was broken trade ties across neighboring countries, including in Central Asia.

This paper takes account of the trade and transit fragmentation induced by the global pandemic and its potential impact on Central Asia’s economic integration in Eurasia. It begins with the logic of Eurasian integration as elucidated by Kent E. Calder[1] and conditions for it to proceed after the pandemic. It then assesses why the five countries of Central Asia (CA5 = Kazakhstan, Kyrgyz Republic, Tajikistan, Turkmenistan, Uzbekistan) figured only modestly in the landscape of an emerging Super Continent between the European and Chinese growth poles prior to the pandemic, and why a high cost of COVID-19 has been to set that pace back further. Finally, it addresses geopolitical constraints on Central Asian connectivity.

The paper argues that the future lies more in the hands of Central Asian governments than in external powers. COVID-19 could leave lasting scars without serious measures to reduce regional barriers to trade, transit and investment. Uzbekistan holds the key to whether Central Asia will become central to European-Eurasian economic integration. Aside from being the most diversified regional economy, which demonstrated the most enlightened leadership during the pandemic, it is the pivot state in a fulcrum region where great power interests collide.

The Logic of Eurasian Integration

Until 2020, evidence of an emerging Super Continent between the growth poles of Europe and China was compelling. As Calder argues, the contours took shape after several critical developments. EU enlargement and the collapse of the Soviet Union opened Eurasia for overland transit while Chinese financial stimulus in response to the Global Financial Crisis raised China’s importance in global aggregate demand and as an investor of European assets, particularly in former Warsaw Pact countries. The Ukraine crisis of 2014 then helped cement Russia’s pivot to China. A once slumbering Super Continent awoke to its privileged geographical coherence, stimulated by energy trade, the Logistics Revolution, and transport financing by BRI and international financial institutions. At one-third of the distance by sea, companies increasingly reaped the benefits of the land bridge for shipment of a range of products. As distanced collapsed, potential for the reconfiguration of Eurasia’s role in world affairs grew. The logic of Eurasian integration was measurable in the three-fold increase in Chinese freight transport[2] in cross-continental trade over the past decade and the reduction of travel time from Xi’an, China to Hamburg, Germany, a 9,400-kilometer journey, to 10-12 days.

COVID-19 cut through that logic like a lightning bolt. The economic drivers of Eurasian integration all suffered setbacks, triggering political tensions. In the Europe and Central Asia region, the World Bank forecasts that exports will decline by 11.8% and imports by 10.7% in 2020.[3] By force majeure, China cut gas imports from Central Asia in March 2020 by an estimated 20-25% and Kazakhstan, Uzbekistan and Turkmenistan were asked to share the reduction proportionally. The Eurasian Economic Union (EAEU) comprised of Russia, Kazakhstan, Belarus, Kyrgyz Republic and Armenia and many other countries in Eurasia such as Ukraine and India suspended exports of food staples and vital medical supplies.[4] Labor migrants, a critical component in integration, suffered the sharpest decline of income in recent history and became stranded in destination countries. Notwithstanding the logistical revolution, delays mounted due to epidemiological tests and uncoordinated border closings. Financing for unexpected health expenditures by international financial institutions received priority attention.[5]

Notwithstanding these pandemic-induced shocks — an extreme case of a “critical uncertainty”[6] – the logic of European-Eurasian economic integration will continue in the long term. First, the geographic advantage of the Eurasian route remains for several products, and the pandemic diverted shipments by air and sea to land. Second, after the recessionary impacts of the COVID-19 recede, energy will continue as a driver of continental trade dynamics. Third, in pursuit of national interest, several countries and the EAEU instituted trade facilitation measures, eased tariffs, and exempted vital imports from customs duties.[7] As discussed below, continuation of such efforts would contribute significantly to European-Eurasian integration.

A consensus appears to be emerging in news analyses and among experts such as former World Bank president Robert Zoellick[8] that globalization would be reshaped but not replaced by the pandemic. A primary reason is that China, Russia and the EU sought to retain and expand foreign markets even as they shored up domestic industries. In this context, despite some delays, the strategic logic of BRI will strengthen, according to the Director of Global Geopolitical Analysis, Arne Elias Corneliussen. Development of Western China, to equalize income levels, will also remain a strong domestic and national security priority for China.[9]

Economic factors influencing integration

While the logic of integration remains strong, two major economic factors that will influence the pace of Eurasian integration are the availability of capital for infrastructure investment and decisions by firms to choose rail rather than sea for long-distance trade. Geopolitical uncertainties, also significant, are discussed below.

Based on previous experience, the global recession is likely to reduce investment, break trade linkages, and weaken supply chains.[10] OECD estimates that global FDI flows may fall by 30% in 2020 and investors will have lower appetite for emerging market risks.[11] In March 2020, investors pulled a record US$83 billion from emerging markets.[12] It is unlikely that China will play the same fiscal stimulus role as it did after the Global Financial Crisis, given domestic needs in China.

Competition for scarce capital will put a higher premium on prioritizing hard infrastructure investments. Decisions are likely to be political as much as economic. Currently there are three routes that traverse Eurasia on an East-West trajectory between China and Europe: northern (through Russia and Belarus), central (through Kazakhstan, Russia and Belarus) and southern (through Kazakhstan to the Caspian). From an operator’s perspective, the northern route by rail is most desirable due to fewer number of countries involved, leading to a reduction in delays at border crossing points and complexity from multimodal transshipment from train to ship to truck.[13] The northern route also benefits from rail electrification and a two-track line. The southern route to Turkey and Southern Europe via the Caspian entails ferry crossings at either Aktau (Kazakhstan) or Turkmenbashi (Turkmenistan) and logistical challenges to cross the rugged terrain of Eastern Turkey. [14]

Investment choices will influence the path-dependence of development. The alternative is to upgrade infrastructure through Russia only, or through Western China through Kazakhstan. The investment decision will depend on demand from manufacturers to ship via rail or road. Thus, infrastructure and manufacturing investments will become co-dependent. Nathan Hutson argues there will not be sufficient demand for both routes, pitting manufacturing firms in Russia against those in Central Asia. Which path will prevail? The outcome will determine investment in warehousing, transport links, and urban agglomeration.[15] There is a political as well as economic dimension: the choice pits winners against losers.[16]

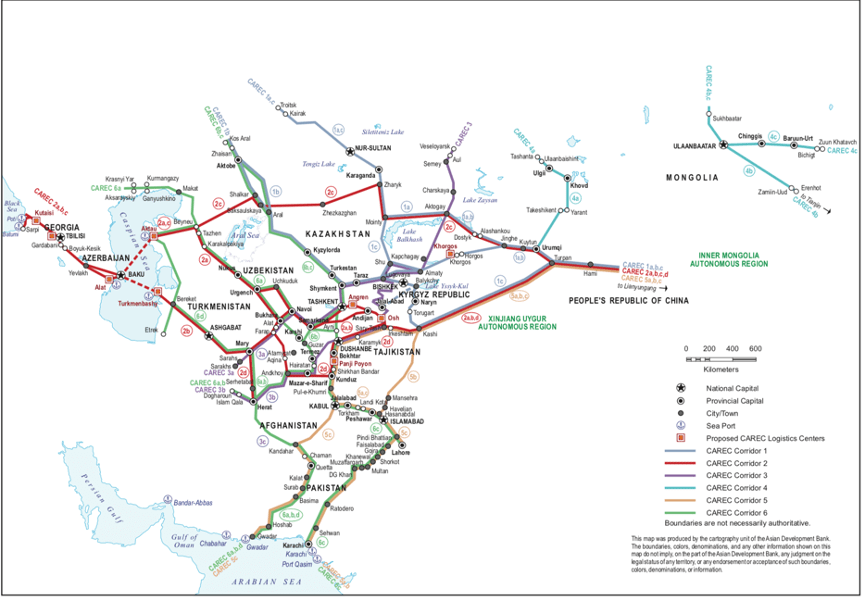

With a superhighway and rail corridor on the Western European-Chinese route, Kazakhstan would appear to be the king of connectivity, holding the most strategic location. The rest of CA5 is crisscrossed by 26 of the 36 incomplete Central Asian Regional Economic Cooperation (CAREC) rail and road corridors, both east-west from China to Europe and north-south from Russia to Iran (Map 1).

Map 1. Six CAREC Transport Corridors

Source: Asian Development Bank in Central Asia Regional Economic Cooperation (CAREC) 2020, p. 2

However, Kazakhstan’s position as a strategic rail line benefits from Chinese container train subsidies. These contributed to the 20% annual growth in rail cargo by container from 2016-2019, or 11% of all freight traffic. Subsidies diverted sea shipments to land as many local governments falsified cargo contents in order to qualify for rail freight subsidies. The Chinese Ministry of Finance will phase the subsidies out in 2022, creating uncertainty over demand for the route.[16] It is not clear if the market would revert to patterns of the past or continue growing albeit at a slower pace,[17] also due to lower global growth post-pandemic.

In addition, the efficiency of transport by rail depends on two-way trade. If high-value goods are not time urgent and only travel in one direction, there is less incentive to ship over land rather than by sea. For example, daily express trains between Duisburg carrying items such as luxury automobiles, wine, and e-commerce parcels from Europe to Chongqing (China) are now possible due to the increase of eastward traffic to China, thus reducing overall rail rates and cost of transit.[18] Interruption of trade flows on a balanced, two-way circuit will have the opposite effect, raising transport costs through reduced cargo freight and shipment frequency. The disruption of supply chains by COVID-19 could put the economics of this trade route under a cloud.

Thus, while the potential for a Super Continent remains valid over the longer term due to geographic coherence, resource endowments, and market complementarities, the pace is contingent on demand by economic actors and investment decisions by governments. The question here is whether the CA5, the geographical “pivot” of Eurasia, can participate in the future as a manufacturing hub rather than a transit zone. I argue that it can. To do so, Central Asian states need to address the home-grown policies that thwart economic diversification.

Connectivity of Central Asia

Trade and Investment Before COVID-19

Until the late Gorbachev period, the Sino-Soviet split separated Central Asia from centuries-long cultural and trade ties with Western China. What could have become a thriving region based on kinship, natural endowments and trade became a frozen landscape of underdevelopment. Decades of disconnect contributed both to China’s decision to opt for a maritime rather than an overland trade route and to high freight transportation costs to reach Central Asia. “In many ways, China’s BRI outreach is an attempt to exorcise the ghosts of the Sino-Soviet split….”[19]

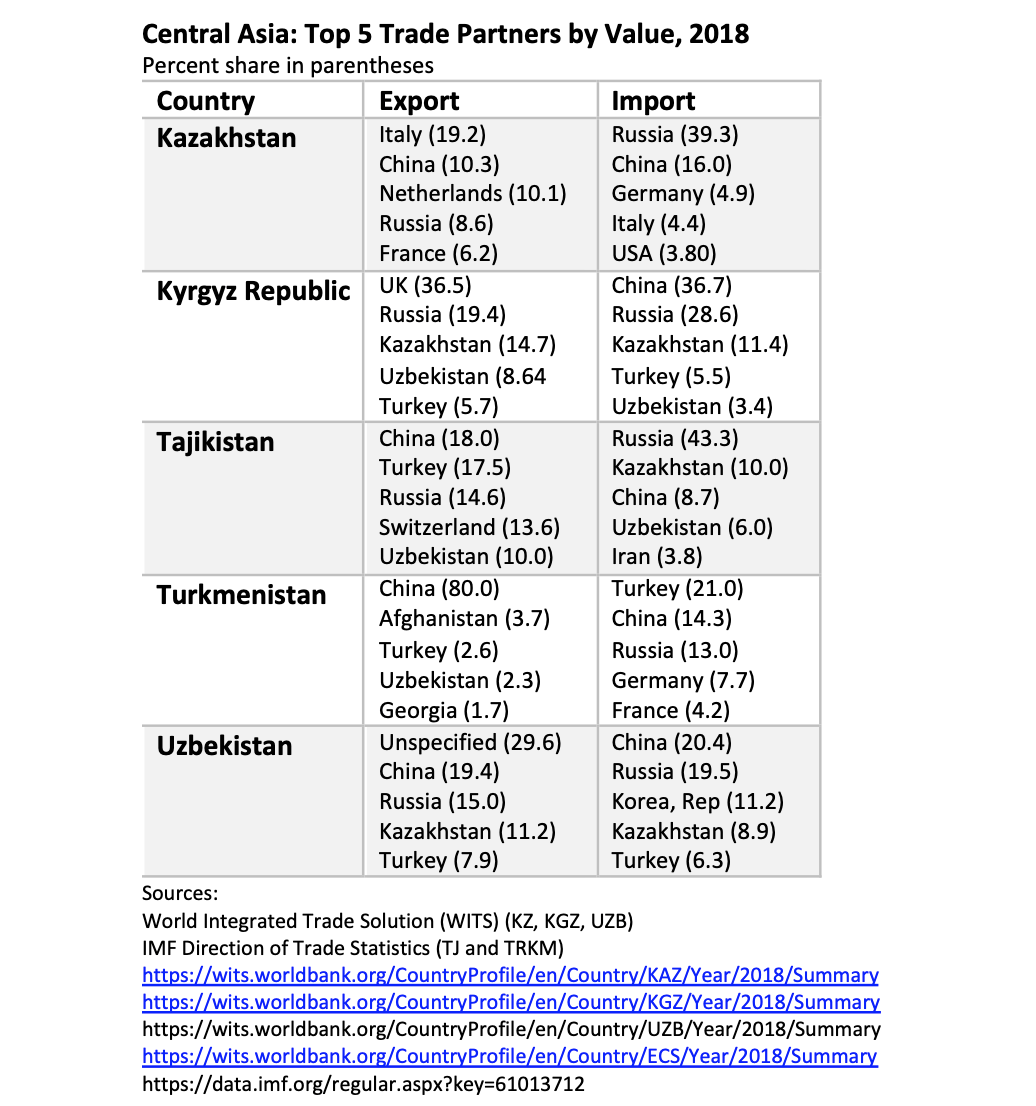

Before the COVID-19 crisis, Central Asian leaders faced an existential choice: either make serious efforts to join global value chains linked to Europe or remain dependent on Chinese and Russian markets. Despite its proximity to the world’s most dynamic markets, and expansion to new partners such as Turkey, integration of Central Asian countries into global value chains (GVCs) was limited. Russia and China figure in the top five trading partners for all of the Central Asian states (Table 1).

Table 1.

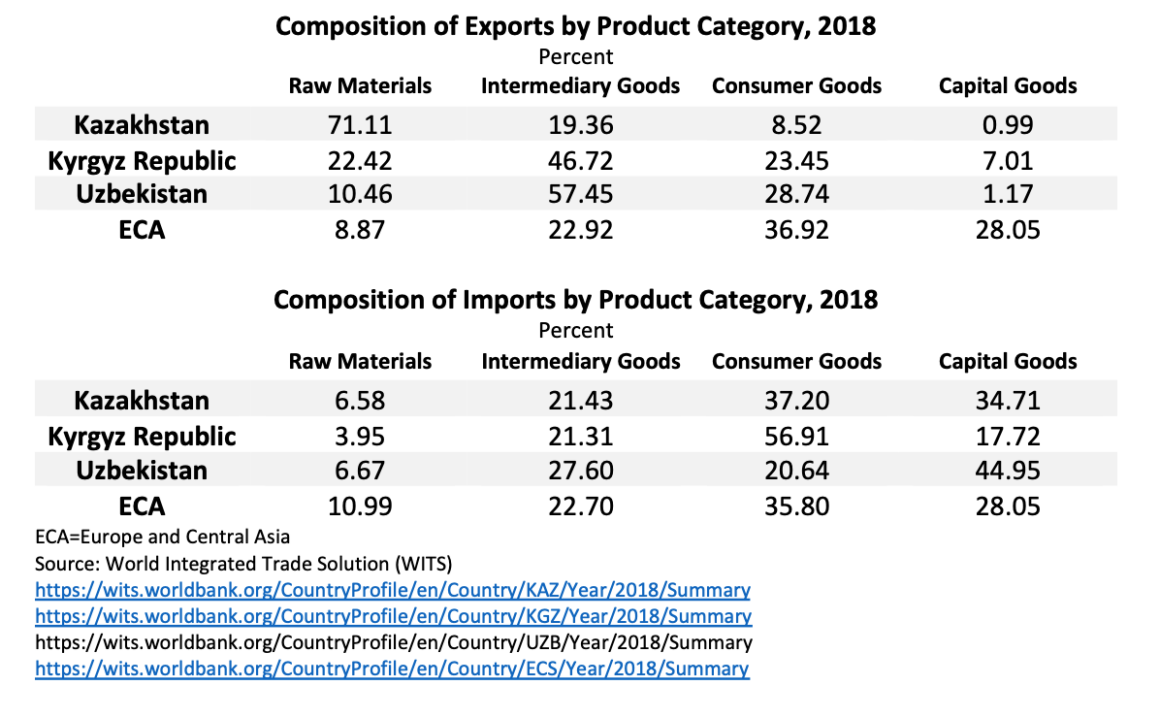

One reason for limited economic integration is a narrow trade basket. Exports are predominantly bulk primary commodities rather than time-sensitive, high-value manufactures, reflecting national asset endowments in metals, minerals and labor (Table 2). A second is high transit cost. Due to complex topography, long distances, low economic density and fragmented trade regimes, it cost 80-150% of the value of goods traded to reach internal markets in 2014, compared to 20% in the EU.[20]

Table 2.

Even prior to the COVID-19 crisis, complex procedures and arbitrary border crossing delays made shippers think twice before using Central Asian routes. Predictability is important for operators. For example, both the time and cost to transit Kazakh borders by road rose in 2019 primarily due to unannounced anti-smuggling procedures in March-April as Kazakh officials inspected vehicles for Chinese goods at the Kazakh-Kyrgyz border crossing point of Karasu. Delays of 34.4 hours were clocked compared to a 0.3 hour wait in 2018, while shippers complained of paying fees of $500 or $1,000 per truck to secure release of goods. As a result, crossing fees rose on average from US$16 to US$101. The issue was resolved through negotiations on April 8, but Kazakhstan’s performance declined significantly on CAREC trade facilitation monitoring indicators[21] This case is also noteworthy as it occurred on an internal border of the EAEU.

Karasu is not the only example of rent-seeking behavior on routes through Central Asia. CAREC monitors unofficial payments annually. In 2019, these broke down according to a similar pattern in 2018: “(i) vehicle registration (52%), (ii) phytosanitary activities (30%), (iii) health and quarantine (29%), (iv) customs controls (25%), and (v) transport inspection (23%).”[22] The highest bribe cost per truck ($92) was for Custom Controls. Corridor 5 from China-Tajikistan-Pakistan registered the highest bribe cost for Custom Controls in 2019 ($105) followed by Corridor 2, which crosses China to the Caspian via Tajikistan, Kazakhstan and the Kyrgyz Republic ($54).[23]

Transit is also complicated by unnecessary requirements for transloading. As explained by CAREC, “[u]nlike the European Union, where trucks, goods, and people can move with minimal border formalities, Central Asian republics tend to require foreign-registered trucks, especially those from Afghanistan, the People’s Republic of China, and Pakistan to stop at the border and transfer the shipment. Due to the generally modest number of containerized shipments, transloading is a complex and time and cost-consuming process.[24]

Clearly it is not enough to build transport corridors if goods and people cannot cross borders easily. These internal trade barriers are among factors that discourage foreign direct investment, a critical lubricant for economic diversification. With the exception of a four-fold increase from 2017 to 2018 in Uzbekistan following trade and economic liberalization, FDI was trending downward across the region, as it has elsewhere since the Global Financial Crisis (Table 3).

Table 3.

Source: https://unctad.org/en/Pages/DIAE/World%20Investment%20Report/Country-Fact-Sheets.aspx

Impacts of COVID-19 on Trade and Transit[25]

Central Asia’s economic structure accentuated the downturn caused by COVID-19 while border closings and new procedures snarled transit. By exposing these deep-seated deficiencies, the pandemic made the region even less attractive for foreign investors than it was prior to the crisis. Yet to recover, diversify economically, and take advantage of its strategic location on North-South and East-West trade routes, FDI is precisely what the CA5 need.

First, the pandemic shock hit the CA5 with a one-two economic punch as global demand fell for the region’s primary exports, commodities and migrant labor, and triggered negative spillovers from key trading partners. For example, Kyrgyzstan is likely to lose 45-50% of expected customs revenue in 2020 due to closing of the borders and secondarily, to the loss of tax payments indirectly linked to border closings. The reduction of imports (70% are from China) strongly impacts domestic production since it is not possible to obtain production components. All countries in the region will contract severely: Kazakhstan (4.5% to -3.0%), the Kyrgyz Republic (4.5% to -4%), Tajikistan (7.5% to -2%), Uzbekistan (5.6% to 1.5%), and Turkmenistan (6.3% to 0.0%).[26] Trade data for the first quarter of 2020 compared to 2019 (Table 4) demonstrate significant market disruption, with the most severe impact in Uzbekistan and Tajikistan on exports and on Uzbekistan and Kyrgyzstan on imports. The increase in Kazakh exports may be attributed to oil (via pipeline) prior to the Chinese reduction.

Table 4.

Trade Turnover in Central Asia

Percent change, Jan-March 2020 vs. 2019

| Exports | Imports | |||||

| Q1 2020 | Q12019 | YoY % Change | Q1 2020 | Q12019 | YoY % Change | |

| Uzbekistan | 3,374.7 | 3,788.2 | -10.92% | 4,765.7 | 5,276.3 | -9.68% |

| Tajikistan | 204.6 | 243.9 | -16.10% | 831.4 | 719.8 | 15.50% |

| Kazakhstan | 13,908.5 | 13,347.9 | 4.20% | 7,098.5 | 7,105.6 | -0.10% |

| Kyrgyzstan | 460.2 | 464.0 | -0.82% | 904.2 | 1,156.5 | -21.82% |

Sources:

- The Republic of Uzbekistan State Committee for Statistics. https://stat.uz/ru/press-tsentr/novosti-komiteta/8896-vneshnetorgovyj-oborot-v-respublike-uzbekistan-yanvar-mart-2020-goda

- National Statistics Committee of the Kyrgyz Republic. Express information, 5/13/2020, http://stat.kg/ru/statistics/vneshneekonomicheskaya-deyatelnost/

- Socio-economic development of the Republic of Kazakhstan. April 2020, Page 16-18, https://stat.gov.kz/edition/publication/month?lang=ru

- Agency for Statistics under the President of the Republic of Tajikistan. Socio-economic development report: Jan-Mar 2020, Page 252

Second, uncoordinated border closings and health procedures contributed to confusion and delays for vital truck freight. [27] Several crossing points at borders with the Kyrgyz Republic, Uzbekistan, China and Russia reopened but were listed as temporarily closed from April 4, 2020. Chines and Kazakh media provided conflicting status reports on Khorgos at the Chinese-Kazakh border. Apart from COVID-related epidemiological delays, Tajikistan and Turkmenistan continued the disruptive practice of requiring customs escorts for foreign trucks or transfer of truck drivers from foreign to national origin at the border. As of June 2020, borders began to reopen, but bottlenecks recurred at the Kazakh-Kyrgyz border.

Integrating into global value chains makes sense for Central Asia

Notwithstanding the current disaffection with supply chains broken by COVID-19, it makes good development sense for Central Asia to leverage its location and natural endowments and increase connectivity to value chains in the dynamic growth poles of Asia and Europe. Prior to the coronavirus crisis, almost half of world trade involved the production of intermediary and final goods through global value chains (GVCs). A 1 percent increase in participation in GVCs raised per capita income by more than 1 percent, which is about twice as much as standard trade.[28] Given its low participation to date in GVCs, Central Asia stands to gain by positioning itself for access to new markets by diversifying from low value-added commodities to manufacturing and accessing new export markets.[29] The region compares favorably with emerging Europe on perceptions of non-price competitiveness except for human capital, on which it exceeds emerging Asia. But trade and transport costs present a high barrier.[30]

From a transport connectivity perspective, three scenarios are feasible: (i) retain a limited niche role as a transit region for goods that are more competitive by land than sea or air; ii) lose traffic due to removal of Chinese subsidies or political conflict along BRI corridors; or iii) become more competitive for freight over land than by sea or air.[31]

Each of these scenarios come with economic development implications. In the first, Central Asian growth would largely be reliant on resource rents and subject to global commodity price shocks. The second is largely outside the control of regional governments. The last has the greatest upside potential and could also mitigate the impact of full transport cost pricing (without Chinese subsidies). By becoming more trade and transit friendly, Central Asia would also become more competitive for foreign direct investment because the freer flow of goods reduces production costs within a larger regional market.

While it is the most optimistic scenario, increasing competitiveness will be more challenging following the COVID-19 crisis. Central Asian governments must address daunting domestic political economy constraints[32] while facing headwinds from lower global growth and risk appetite for investment in emerging economies. A starting point is for Central Asian governments to reduce trade and transit barriers through policy coordination.

Regional Coordination and the Role of Uzbekistan

Prior to COVID-19, the reversal of regional tensions held promise for policy coordination. Following nearly a decade of tense relations, President Nazarbayev of Kazakhstan convened an historic summit in March 2018 that was the first meeting of in Central Asian heads of state on a broad agenda since 1999. A second summit followed in November 2019 in Tashkent. Then the pandemic struck. Borders closed and trade barriers mounted for critical food and medical supplies.

Against expectations, dialogue countered the disruptive effects of COVID-19. As reported in regional media, Presidents Mirziyoyev of Uzbekistan and Jeenbekov of the Kyrgyz Republic discussed mutual support measures in late March 2020. In early May, Mirziyoyev and President Rahmon of Tajikistan agreed to keep trade flowing. Similar coordination efforts took place between Mirziyoyev and President Tokayev of Kazakhstan. On May 19, 2020, at the invitation of the Uzbek Minister of Agriculture and FAO, all CA5 agriculture ministers (notably including Turkmenistan) met to discuss pandemic-related logistical disruptions to food distribution and agricultural trade in the region, with participation of EBRD, ADB, and the World Bank. As a result of the meeting, each country has designated a focal point to examine food security and phytosanitary measures, opening a door to improve conditions for agricultural trade.[33]

Mirziyoyev’s effort to reconnect the region is undeniably game-changing. The first summit resulted from his initiative and capped a series of bilateral efforts to normalize relations (most significantly with Tajikistan), demarcate contentious borders, open new border crossings and transport links, and harmonize customs regimes (between Uzbekistan and Kazakhstan, and Uzbekistan and the Kyrgyz Republic). During the COVID-19 crisis, actions by the Uzbek president to call his neighbors, resist food export bans, promote trade dialogue, and resolve cross-border freight delays demonstrated deft political leadership. The August 27, 2020 announcement that Uzbekistan intends to reconnect Tajikistan and Turkmenistan to the Central Asian Power System (CAPS) will eventually generate billions of dollars in fuel savings and unserved energy demands for the entire region.[34]

More broadly, domestic economic reforms since 2018 suggest Uzbekistan will diversify sooner and drive expansion in the now paltry level of regional trade.[35] For example, Uzbekistan rose to become a top five market for exports from the Kyrgyz Republic, Tajikistan and Turkmenistan in 2018. From 2016 to 2018, the value of Tajik exports increased from $6M to $155M. More than Kazakhstan, Uzbekistan holds the key to regional dynamism and attraction of foreign direct investment.

Geopolitical Constraints to Connectivity

Prior to COVID-19, geopolitics complicated regional policy coordination among CA5 countries. China preferred to deal with Central Asian governments bilaterally, with limited disclosure of transactions, while Russia preferred to work through the EAEU, splitting the region between members (Kazakhstan and the Kyrgyz Republic) and non-members (Tajikistan, Turkmenistan and Uzbekistan). In contrast, the EU and US advocated regional cooperation among the CA5, which would enhance their bargaining power vis-à-vis China and Russia. However, with the exception of Kazakhstan, both the EU and US are secondary economic actors in Central Asia and only marginally influential on policy decisions. Central Asians overwhelmingly preferred Chinese infrastructure investments to Western pressure for institutional reforms.

New East-West tensions following the pandemic accentuated these contrasting approaches. Areas of contestation between China and Russia shrank while the gap widened with the West.

China at the Center

China remains the economic driver of Eurasian integration. The economic impact of COVID-19 puts China on track to match the US economy in absolute terms by 2028, according to Homi Karas, a senior fellow at the Brookings Institution.[36] At the same time, while respect for Chinese containment of COVID has overcome criticism of its responsibility for the outbreak, China’s suspension of gas imports from Kazakhstan, Turkmenistan and Uzbekistan will increase Sino-skepticism, particularly if promises by China to reinstate trade and investment do not bear fruit.

The decoupling of the US and Chinese economies that began under President Trump is not likely to abate. Militarily, US Secretary of Defense Esper has declared China the number one antagonist in Great Power competition, supplanting Russia, which once held double billing with its Eurasian neighbor.[37] Indirect tensions between the US and China in Central Asia could become overt.

Russia in the Middle

Being in the middle of the East-West trade route bestows some advantages on Russia. Unlike China, which increased reliance on western-oriented trade, Russia turned to import substitution after the imposition of Western sanctions following Ukraine.[38] This strategy also opens opportunities for imports from Central Asia in the aftermath of COVID-19. According to the EAEU Commission, “[d]espite the decline in world trade, the deterioration in demand, increased risks, and increased protectionism, new opportunities are opening up for the economies of the member states of the Eurasian Economic Union.”[39]

Russian support is essential to the success of the Silk Road Economic Belt (the BRI brand in Central Asia)[40]. That support is likely to strengthen due to the increase in Russian trade turnover with China due to BRI (Table 5).

Table 5.

China-Russia Transit Rail Container Traffic in TEU

2014–2018[41]

EU in the Wings

In a 2016 review of EU strategy in Central Asia, the EU Directorate-General for External Relations stated bluntly that “[t]he EU should not and cannot compete with Russia and China in the region.” The review noted that the EU strategy, dating from 2007, with limited resources (US$750 million from 2007-2013), had suffered from numerous challenges, including political backsliding, corruption, and the failure of Central Asian energy exports to materialize. The report concluded that EU interventions had resulted in “limited to no impact.” [42]

The new EU strategy is grounded in economic fundamentals, starting with support for accession to the WTO (by Uzbekistan), improving trade and transport connectivity, and extending access to the EU Generalized Scheme of Preferences and Partnership and Cooperation agreements. A primary goal of these agreements is to help countries adopt EU standards so as to increase their access to European markets.

This strategy has been upended by COVID-19 and the contested Belarus elections in August 2020. Should the EU decide to impose sanctions on officials who persecuted election protesters, President Lukashenko has promised to retaliate by blocking East-West rail transport.[43] The ability of one country to threaten continental integration could increase demand for routes to the south of the Caspian, putting pressure on Russia to keep the trains running.

US at the Periphery

The US is more than geographically peripheral to European-Eurasian integration; it is increasingly isolated by a failure of policy imagination. Narrow vision, both in security policy and economic development, means the US is unable to influence the evolving Eurasian landscape. Yet in the field of trade and investment, it has numerous opportunities. For example, it could use its good offices to convene stakeholders in Georgia and Central Asia to harmonize shipment costs.[44] It also needs to consider the impact on Central Asia of its sanctions policy. Sanctions on Iran have impacted trade between Central Asia and Iran by diverting transit through Turkmenistan from Bandar Abbas (the preferred port) to Georgia, adding to shipment time and costs.[45]

Conclusion: Uzbekistan as the Pivot

Geopolitical fragmentation is a deterrent to external coordination. As a consequence, progress in cooperation requires greater leadership by Central Asian states and willingness to harmonize national policies. The absence of an institutional framework owned and managed by Central Asians remains a stumbling block to regional coordination.[46]

Uzbekistan is the pivot country. It is under pressure by Russia to join the EAEU as a full member (not just observer, as passed by Parliament); China is neck-and-neck with Russia for dominance as an economic partner; and the new US strategy for Central Asia is now aimed at trilateral dialogue with Uzbekistan and Afghanistan. According to one Uzbek observer, much will depend, on the one hand, on the effectiveness of Washington’s implementation of the new Central Asian strategy, and on the other, on how successfully Beijing will advance its One Belt, One Road initiative.

Within the region, the outlook depends more on actions by Uzbekistan than other l players.[47] Uzbekistan is the most populous and most willing to undertake market-opening reforms. At the peak of the crisis in Spring 2020 it demonstrated the most enlightened leadership vis-à-vis its neighbors, led calls for coordination, and promoted industries aimed at higher-end European markets. Without serious new Western investment in Uzbekistan, Russia and China will continue to dominate, and Central Asia is likely to remain peripheral to European-Eurasian integration.

References

Calder, Kent E. 2019. Super Continent: The Logic of Eurasian Integration. Stanford, California: Stanford University Press.

CAREC. 2020. Corridor Performance Monitoring and Measurement Annual Report 2019. DOI: http://dx.doi.org/10.22617/TCS200205-2.

Hutson, Nathan. 2019. The Development Implications of China’s Belt and Road Initiative for Russia, Kazakhstan and Belarus. Ph.Diss, University of Southern California, Department of Urban Planning and Development.

http://digitallibrary.usc.edu/cdm/compoundobject/collection/p15799coll89/id/167981/rec/1

International Monetary Fund, Washington, D.C.

July 2020. Regional Economic Outlook: Middle East and Central Asia. https://www.imf.org/en/Publications/REO/MECA

October 2019. Regional Economic Outlook: Middle East and Central Asia.

https://www.imf.org/en/Publications/REO/MECA

2018. Direction of Trade Statistics.

https://data.imf.org/?sk=9D6028D4-F14A-464C-A2F2-59B2CD424B85

World Bank, Washington. D.C.

2020. Global Economic Prospects, June 2020. https://openknowledge.worldbank.org/handle/10986/33748

2020. COVID-19 Trade Policy Database: Food and Medical Products. https://www.worldbank.org/en/topic/trade/brief/coronavirus-covid-19-trade-policy-database-food-and-medical-products

2020. Central Asia’s Horticulture Sector — Capitalizing on New Export Opportunities in Chinese and Russian Markets. © World Bank.

https://openknowledge.worldbank.org/handle/10986/33652

2019. Belt and Road Economics: Opportunities and Risks of Transport Corridors. Washington, DC.

2019. World Development Report (WDR) 2020: Trading for Development in the Age of Global Value Chains. https://www.worldbank.org/en/publication/wdr2020

2014. Central Asia: Development through Trade. Poverty Reduction and Economic Management Unit, Europe and Central Asia Region.

[1] Kent E. Calder, Super Continent: The Logic of Eurasian Integration, Stanford, California: Stanford University Press, 2019.

[2] OECD (2020), Freight transport (indicator). doi: 10.1787/708eda32-en (Accessed on 04 September 2020)

[3] World Bank, Global Economic Prospects, June 2020, Table 2.2.1

[4] On food and medical supplies, see World Bank, COVID-19 Trade Policy Database: Food and Medical Products. https://www.worldbank.org/en/topic/trade/brief/coronavirus-covid-19-trade-policy-database-food-and-medical-products.

[5] The World Bank, Asian Development Bank, European Bank for Reconstruction and Development, Eurasian Development Bank, and Asian Infrastructure Investment Bank all provided emergency lending, including on soft terms for low-income countries.

[6] Calder 2019, Chapter 9

[7] Responses by country are available at https://www.tfafacility.org/covid19-trade-facilitation. For the EAEU, see the report to the World Customs Organization by Kazakhstan.

[8] His remarks were delivered at the CAMCA (Central Asia, Mongolia, Caucasus) Regional Forum in Almaty in June 2020.

[9] Hutson, pp. 18-19; Calder p. 115.

[10] World Bank, Global Economic Prospects, June 2020, Chapter 3

[11] OECD, COVID-19 Crisis Response in Central Asia, June 4, 2020, p. 17.

[12] Wall Street Journal, June 20-21, 2020.

[13] CAREC, Corridor Performance Monitoring and Measurement Annual Report 2019, p. 32. This calculation may be affected by political upheaval in Belarus.

[14] Nathan Hutson, The Development Implications of China’s Belt and Road Initiative for Russia, Kazakhstan and Belarus, Ph.Diss, University of Southern California, Department of Urban Planning and Development, 2019, p.37.

[15] Ibid., p. 79

[16] Estimates of economic impacts on winners and losers in Central Asia can be found in World Bank, Belt and Road Economics: Opportunities and Risks of Transport Corridors. Washington, DC., 2019.

[16] CAREC 2020, p. 39

[17] Hutson 2019, p. 45.

[18] Carec 2020, p. 30.

[19] Hutson 2019, pp. 10-12. On the maritime option, see p. 24.

[20] World Bank, Central Asia: Development through Trade. Poverty Reduction and Economic Management Unit, Europe and Central Asia Region, 2014, p. 39.

[21] CAREC 2020 pp. 42-45

[22] CAREC 2020, p. 20

[23] CAREC 2020, Table 4.4, p. 20.

[24] CAREC 2020, p. 23

[25] This section draws on a Working Paper by Marsha McGraw Olive and Cordula Rastogi prepared for the Europe and Central Asia Region of the World Bank.

[26] World Bank, Global Economic Prospects, June 2020.

[27] Impact on freight and passenger transport of the global Coronavirus (COVID-19) outbreak were reported by country at iru.org/covid19.

[28] World Development Report (WDR) 2020: Trading for Development in the Age of Global Value Chains. https://www.worldbank.org/en/publication/wdr2020

[29] Revealed comparative advantage for the CA5 include potential for higher value-added exports in energy, minerals, chemicals, metals, agriculture, and textiles. See IMF 2019, p. 30. Also horticulture holds potential for export to China, Russia and Europe. See China 2030 – Opportunities for Central Asian Agriculture. World Bank (July 2019)

[30] IMF 2019, p. 27.

[31] Hutson 2019, p. 131.

[32] These include high state ownership of industry and low transparency in business. See IMF 2019 and chapters by Lain and Kurbanov in Marlene Laruelle, ed., China’s Belt And Road Initiative And Its Impact In Central Asia. Washington, D.C.: The George Washington University, Central Asia Program, 2018. www.centralasiaprogram.org

[33] Interview with World Bank official.

[34] Central Asia Energy Water Development Program (CAEWDP), Enhancing Energy Power Trade in Central Asia. World Bank Europe and Central Asia Region Report No: ACS21198, July 2016. The system collapsed in 2009.

[35] Only 8 percent of CA5 countries’ trade is with regional neighbors compared to 24 percent in ASEAN, 49 percent in NAFTA, and 64 percent in the EU (UNCTAD Statistics 2018).

[36] Wall Street Journal, August 25, 2020, p. A8.

[37] Mark Esper, “The Pentagon is Prepared for China,” Wall Street Journal, August 25, 2020, p. A17.

[38] Hutson 2019, 23.

[39] These include food and processed agricultural products for markets in China. At the same time, EEC Minister of Trade Andrei Slepnev observed the importance of maintaining markets in the EU. In 2019, 18% of EAEU trade turnover was with China and 44.5% was with the EU.

[40] Hutson 2019, 20-22.

[41] CAREC 2020, 32.

[42] European Union, Directorate-General for External Policies, Implementation and Review of the European Union – Central Asia Strategy: Recommendations for EU Action,” 2016: doi:10.2861/587065 (pdf).

[43] Wall Street Journal, August 29-30, 2020, p. A7.

[44] CAREC 2019, p. 42.

[45] CAREC 2019, p. 55

[46] Bilahari Kausikan, S. Frederick Starr, and Yang Cheng, “Central Asia: All Together Now, “The American Interest,” June 16, 2017. https://www.the-american-interest.com/2017/06/16/central-asia-all-together-now/

[47] This view was also expressed by Luca Anceschi, author of Analysing Kazakhstan’s Foreign Policy: Regime Neo-Eurasianism in the Nazarbaev Era on August 27, 2020 at a discussion sponsored by the Central Asian Program at George Washington University IERES.